Owning a vacant property, whether a building or a parcel of land, does come with a set of unique risks that traditional or standard insurance policies often fail to address. Increased vulnerability to vandalism and weather damage are just some of the reasons why these types of properties require a specialized policy to provide adequate protection. This comprehensive guide, rewritten to stay relevant in 2025 and beyond, explores everything you need to know about vacant building insurance and land insurance – including costs, coverage options and essential tips to make the most informed decisions.

Whether you’re temporarily leaving a property unoccupied, or holding onto an empty lot, understanding your insurance coverage(s) and needs are vital for financial security.

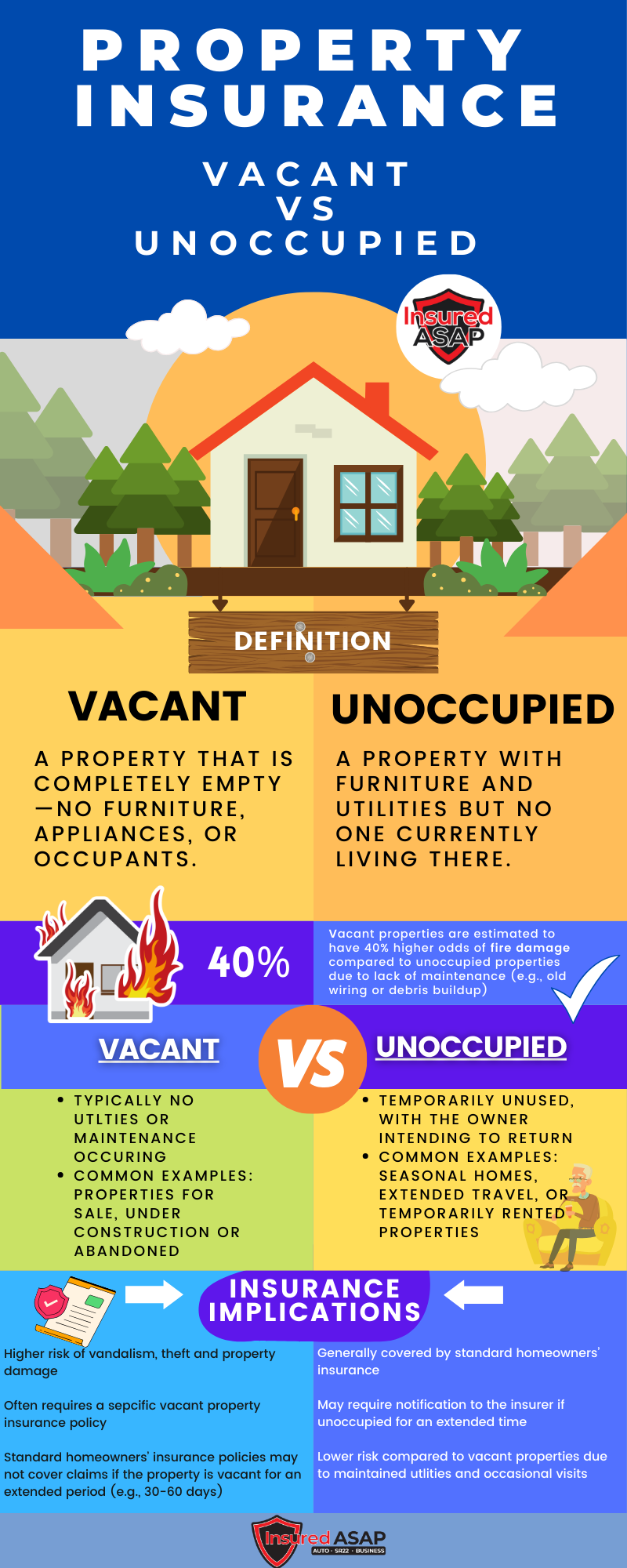

What Is Vacant Building Insurance?

Vacant building insurance is a specialized type of coverage designed to protect properties that are unoccupied for an extended period. Unlike standard property insurance, which assumes occupancy, vacant building insurance addresses the unique risks associated with unoccupied properties, such as vandalism, theft, and undetected damage.

A property is considered “vacant” if it is entirely unoccupied and does not contain enough furniture or personal property to be livable. On the other hand, an “unoccupied” property is one that is temporarily empty but still maintained. Understanding this distinction is critical when determining the type of coverage needed for your property.

Why Is Vacant Property Insurance So Expensive?

Insuring a vacant property often costs more than standard property insurance due to the increased risks:

- Vandalism and Theft: Empty buildings are more susceptible to break-ins and vandalism. Without regular activity, these properties become targets for unlawful activity.

- Undetected Damage: Issues like water leaks, mold, or fire can go unnoticed for extended periods, resulting in more extensive and costly damage.

- Liability Risks: If someone is injured on the property, even without permission to be there, the owner can still be held liable.

Insurance companies charge higher premiums to offset these elevated risks. Additionally, vacant property policies often include stricter terms and conditions, which can further increase costs.

Vacant Property Insurance for Areas of High Crime

Generally speaking, businesses located in an area with a high crime rate typically come with higher than normal insurance costs. This is also true for vacant homes and commercial properties. High crime areas, such as certain parts of Chicago, IL., Houston and San Antonio, Texas, and parts of Florida such as Jacksonville, typically come with added risks of crime, such as deteriorating structures, theft, trespassing, etc. Find your crime statistics here.

Generally speaking, businesses located in an area with a high crime rate typically come with higher than normal insurance costs. This is also true for vacant homes and commercial properties. High crime areas, such as certain parts of Chicago, IL., Houston and San Antonio, Texas, and parts of Florida such as Jacksonville, typically come with added risks of crime, such as deteriorating structures, theft, trespassing, etc. Find your crime statistics here.

How to Insure a Vacant Building

To ensure adequate coverage for your vacant building, follow these steps:

- Determine Your Needs: Assess the property’s condition, location, and how long it will remain vacant. Consider any planned renovations or changes to the property’s use.

- Compare Policies: Look for the best vacant building insurance policies that suit your needs and budget. Policies can vary significantly in terms of coverage and exclusions. Our agency can help shop multiple A rated national insurance carriers to find the best vacant building insurance policy.

- Consider Builders Risk Insurance: If the property is undergoing renovations or construction, builders risk insurance might be a more suitable option. This type of coverage protects materials, equipment, and construction-related risks.

- Work with Specialists: Choose vacant home insurance companies with experience in this niche. Our agents at Insured ASAP can help you navigate the complexities of coverage.

- Maintain the Property: Insurance providers may offer lower premiums if you take proactive measures, such as installing security systems, disconnecting utilities or scheduling regular inspections.

Average Monthly Cost of Vacant Property Insurance

Vacant property insurance premiums vary widely depending on the property type (residential, commercial, or industrial), location, building condition, year built, and the property’s intended use. Other key rating factors include the year of last updates (roof, electrical, plumbing, HVAC), security measures, and how long the property is expected to remain vacant.

Below is a sample breakdown of estimated monthly costs based on property value and state. These are general estimates and can vary depending on underwriting details:

| Property Value | Illinois (IL) | Indiana (IN) | Missouri (MO) | Wisconsin (WI) |

|---|---|---|---|---|

| $200,000 | $110/month | $95/month | $105/month | $100/month |

| $400,000 | $170/month | $145/month | $155/month | $150/month |

| $600,000 | $230/month | $200/month | $215/month | $205/month |

| $1,000,000 | $370/month | $320/month | $340/month | $330/month |

| $1,500,000 | $525/month | $465/month | $490/month | $480/month |

| $2,000,000 | $680/month | $600/month | $630/month | $615/month |

💡 Tip from the pros: Pricing is often higher for older properties or buildings with outdated electrical/plumbing systems, no active renovations, or those located in urban zones with high claim frequency. You’ll get better pricing if you have a plan in place to renovate, lease, or sell the building within 3–12 months.

Builders Risk Insurance

If your vacant building is undergoing construction or significant renovations, builders risk insurance might be a better fit. This policy typically covers:

- Materials and supplies

- Tools and equipment on-site

- Damage from fire, theft, or weather events

- Liability for accidents during construction

Builders risk insurance is usually a temporary policy, active for the duration of the construction project. Discuss this option with one of our agents today to ensure comprehensive protection.

Vacant Land Insurance: A Necessity for Landowners

What Is Vacant Land Insurance?

Vacant land insurance is a liability-focused policy designed to protect landowners from legal and financial risks. While the land may not have structures or ongoing activities, it still poses potential hazards, such as:

- Natural features like ponds or uneven terrain

- Unintentional trespassing by hikers or hunters

- Environmental risks, such as erosion or wildfires

Do I Need Insurance on Vacant Land?

Even if your land is undeveloped, vacant land insurance is essential for the following reasons:

- Liability Protection: If someone is injured while on your property, you could be held legally responsible, even if they were trespassing.

- Peace of Mind: Insurance ensures that you are financially covered in case of lawsuits or unforeseen events.

Many lenders require vacant land insurance as a condition of financing. Even if it’s not mandatory, it’s a smart investment to mitigate risk.

How Much Does It Cost to Insure Vacant Land?

The cost of insuring vacant land is generally lower than insuring buildings. Key factors influencing the cost include:

- Size and Location: Larger parcels of land or those in high-risk areas (e.g., flood zones) may have higher premiums.

- Intended Use: Land intended for future development may require additional coverage.

- Proximity to Urban Areas or Public Access: Properties near public roads or recreational areas may pose higher liability risks.

On average, vacant land insurance premiums range from $100 to $500 annually, depending on these factors and the coverage limits selected.

How to Insure Vacant Land

To insure your vacant land effectively:

- Evaluate Risk Exposure: Consider liability risks, such as unauthorized access or natural hazards like flooding or erosion.

- Choose Appropriate Coverage: Basic liability insurance is typically sufficient for most vacant landowners. Additional coverage may be needed for higher-risk properties.

- Shop Around: Compare quotes from multiple providers to find the best policy for your needs.

- Bundle Policies: If you own other insured properties, consider bundling policies to receive discounts.

Common Questions About Vacant Land Insurance

How Much Is Property Insurance on Vacant Land?

The cost varies widely based on factors like size, location, and intended use. Most policies are affordable, with premiums ranging from $100 to $500 annually.

What Does Vacant Land Insurance Cover?

Vacant land insurance typically covers:

- Liability for injuries occurring on the land

- Legal fees related to claims

- Damage caused by natural events, depending on the policy

Can I Extend My Homeowner’s Policy to Cover Vacant Land?

In some cases, you may be able to add vacant land coverage to your existing homeowner’s insurance policy. Check with your insurance provider to explore this option and ensure it meets your needs.

By understanding the nuances of both vacant building insurance and vacant land insurance, you can make informed decisions to protect your investments effectively. Whether you’re insuring an unoccupied property or safeguarding an empty parcel of land, the right coverage provides peace of mind and financial security.

Vacant Property Insurance Quotes

Insured ASAP Insurance Agency partners with the nations largest insurance providers and helps property owners find the best building insurance. Whether you’re in search of builders risk, vacant property, vacant home or vacant land insurance, our agents can help find an affordable policy to meet your specific needs. Our agency is licensed to provide coverage in the following states:

- Alabama

- Arizona

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Michigan

- Minnesota

- Missouri

- New Mexico

- Ohio

- Oklahoma

- Texas

- Virginia

- Wisconsin

Get started on your vacant property insurance quote online, by phone call or text messaging.